Menu

Close

Menu

Close

April 28, 2025

During the first quarter of 2025, the Fairlight Fund declined 2.2%, slightly less than its benchmark, which fell 2.4%. Global markets have continued falling through April, as investors attempt to quantify the negative impact of escalating trade frictions on global economic growth, inflation and interest rates.

The Fund’s outperformance has widened so far this month. At the time of writing (8 April 2025), the Fund is down approximately 4%, while the index is down approximately 7%. Fairlight’s better relative performance is mostly due to our quality investing approach, where we prioritise resilient businesses with strong balance sheets and proven track records that can perform well through the cycle, even during economic recessions. The Fund’s performance has also been helped by a slightly higher exposure to European companies versus the benchmark.

In these turbulent times for markets, the resilience of the portfolio is allowing the investment team to remain focussed on assessing businesses’ competitive advantages and identifying new opportunities rather than having to reposition the portfolio for likely more challenging economic times.

In this monthly report, we will:

• briefly summarise the recent business performance of the Fund’s investments;

• discuss how the recent trade frictions might impact their operations; and

• outline how the Fund is positioned to try to continue to deliver superior risk-adjusted returns over the long-term.

Earnings performance in Q4 2024

Over the past two months portfolio companies reported their most recent quarterly results (Q4 2024). Out of the 35 holdings, 22 reported results that were in line with our estimates, five above and eight below.

The number of companies beating our expectations was slightly below the historical average mainly reflecting weaker performance across the industrial companies within the portfolio and most companies guiding for a challenging 2025 (Figure 1). Overall though it was a pleasing reporting season.

Figure 1. Q4 2024 result sentiments vs history

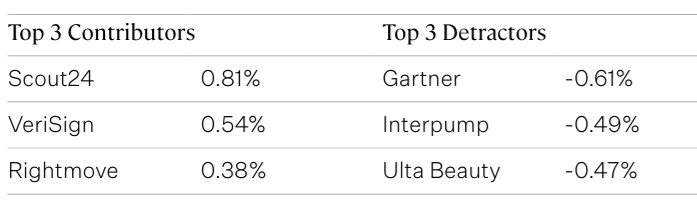

Online property portal Scout24 was the largest positive contributor to Fund performance over the quarter while research provider Gartner was the largest detractor (Table 1).

• Scout24 is the dominant player in Germany with a 65% market share. The business saw positive trends in nearly all its KPIs in Q4. Management pleasingly upgraded organic growth expectations from high-single to low-double-digit, while maintaining margin expansion.

• Gartner provides specialised data and research to executives of large corporates and it is the clear leader in this niche generating ten times more sales than its closest peer. Gartner delivered 2024 EPS growth, 6% above our estimate but later in the quarter the US federal government announced it will likely reduce its number of Gartner subscriptions meaning that Gartner might no longer be able to meet its annual guidance in 2025.

Table 1. Contribution to returns Q1 2025

Two new investments were made in the quarter and three completely sold, two-based on valuation and one due to thesis drift. This level of activity is consistent with the history of the Fund. The Fairlight process directed us to review our holding in Spirax Group, the owner of a great industrial steam business which is over 100 years old. Our team conducted a full review of the thesis and identified drift and were able to sell this position and reallocate capital to better ideas. Market volatility allowed us to initiate a position in IDEXX Laboratories, a business which we have followed and researched for a long time and have profiled in last month’s update.

Escalating trade wars and inflation risk

We estimate that about 80% of the portfolio has little to no impact by the tariffs proposed by the new US administration. About 18% is moderately impacted and only 2% significantly impacted (Figure 2).

Power tools manufacturer Techtronic Industries, is the Fund’s most exposed business, generating 80% of its sales in the US but manufacturing most of its components in China and Vietnam. Importantly, Techtronic remains the global market leader in the structurally growing niche of cordless tools, and has proven in the past (and under previous tariff regimes) to be able to gain market share during challenging periods.

Figure 2. Direct tariff impact

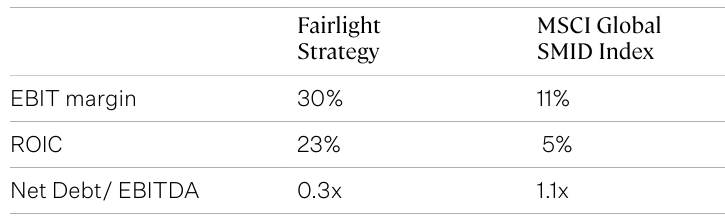

At Fairlight, pricing power is the number one input to our models, and thus we believe our portfolio companies should be relatively well-placed to weather the inflationary impact of tariffs and potentially higher interest rates. In an inflationary environment it is businesses with low operating margins that face the greatest earnings risk. Currently the portfolio average operating margin sits at 30%, almost 20 percentage points higher than the average index constituent. In 2023, our portfolio companies demonstrated margin resilience in an inflationary environment, and we expect to see similar evidence going forward.

The average portfolio company has minimal amounts of debt with only 0.3x net debt to EBITDA, significantly lower than the average index constituent of 1.1x, meaning they will be much less impacted if rates rise (Table 2).

Table 2. Portfolio metrics

Portfolio positioning

If global recession was to ensue, we still believe that the portfolio will prove relatively defensive. The Fairlight strategy focuses on capital preservation by removing as much fundamental risk as possible, which also involves excluding sectors that are highly levered, highly regulated and macro dependent.

The portfolio is invested in sectors where growth is sustainable and businesses that are relatively easy to model where the variability of outcomes is relatively narrow. As shown earlier in the report, the great majority of our companies end up reporting results that meet our expectations (Figure 1). This translates to a portfolio that is heavily skewed towards more ‘defensive’ sectors such as healthcare and almost not exposed at all to ‘the consumer’ (Figure 3).

Figure 3. Portfolio positioning

The Fairlight View

During periods like this, it’s natural to question whether investment strategies should shift in response the changing conditions. At Fairlight, we believe that long-term wealth is achieved through consistent, disciplined decision-making and careful risk management and so we remain committed to our philosophy of owning a concentrated portfolio of 30 to 40 high-quality small and mid-cap companies, selected with valuation discipline and a long-term mindset. Looking ahead, the team will be active on the ground, with members spending prolonged time across Europe, the UK and the US to deepen engagement with our investments and explore new opportunities. Following overwhelmingly positive feedback on our recent webinar, we would like to take the chance to sincerely thank our investors for their continued support.