Menu

Close

Menu

Close

June 15, 2026

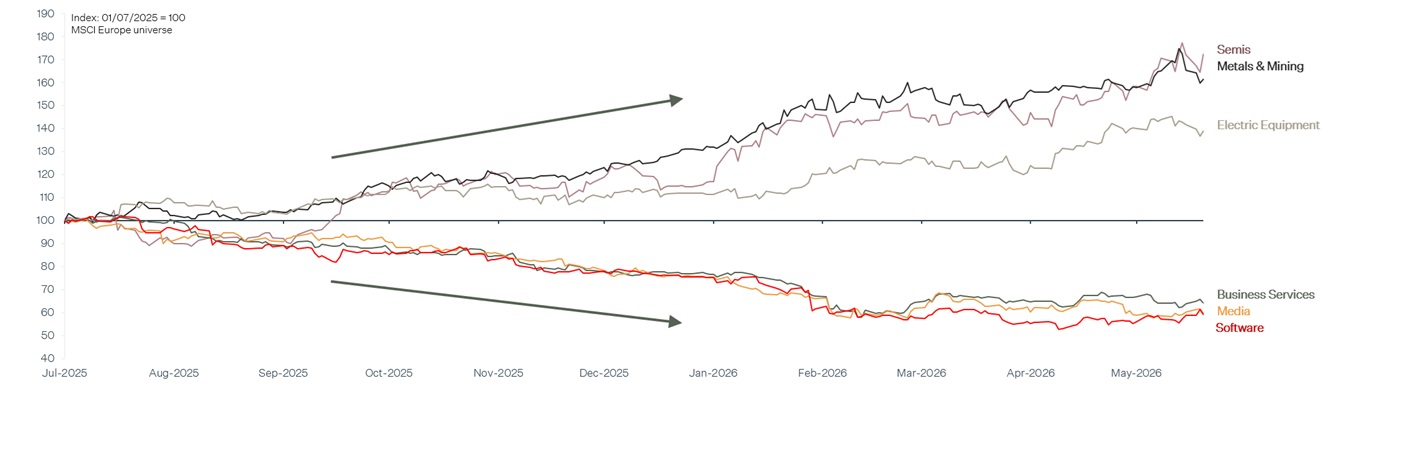

The Fund’s benchmark rose 3% in May, 3 points higher than the flat net return of the Fund. The gap in performance is almost entirely explained by the soaring share prices of semiconductor companies, the chief beneficiaries of the fast-growing investment that is going into AI-infrastructure (Figure 1). Several Fairlight holdings have been benefiting from this trend as they are selling some of their products and services into these end-markets (e.g. construction and fit out of data centres and specialised equipment for chip manufacturing). However, the diversified earnings profiles of these Fund holdings have not attracted the equivalent explosive multiple expansion that we have seen for a narrow set of semiconductor companies within the index.

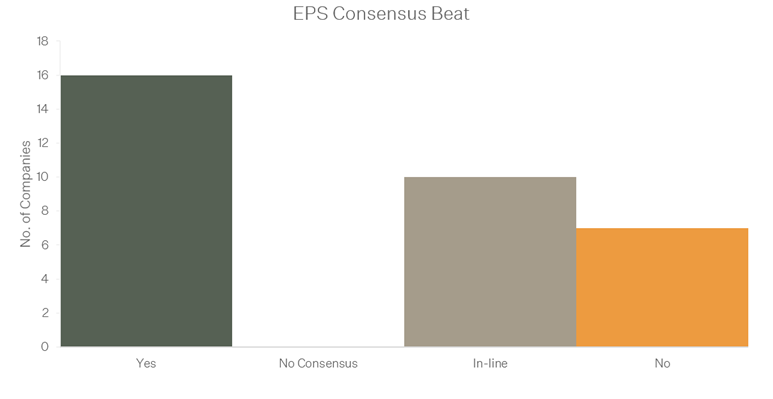

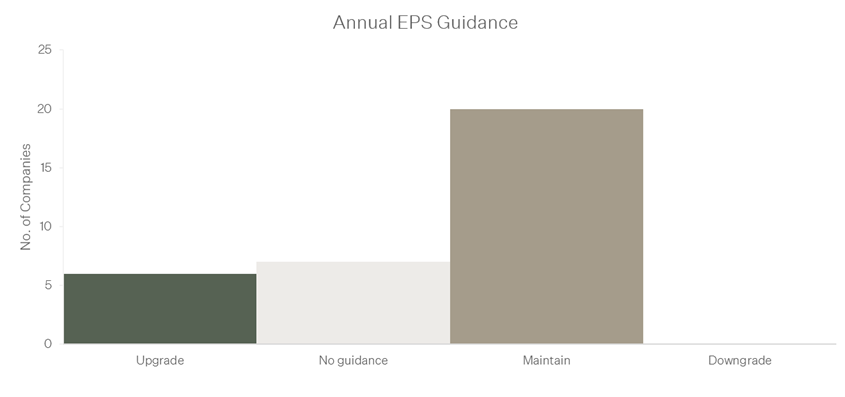

Despite this, the Fairlight portfolio remains on track for another year of double-digit Earnings Per Share (EPS) growth, targeted in a low-risk way and in line with the long-term average of 12-13% per annum. The first reporting season of 2026 has just concluded, and the great majority of portfolio companies reported EPS growth either in line with market expectations (10 out of 33 companies) or above market expectations (16 out of 33 companies). Importantly, despite ongoing geopolitical tensions, the management of every portfolio company has either maintained or upgraded its annual EPS guidance (Figure 2 and Figure 3). Some of the most recent results are highlighted below, along with a new addition to the Fund.

Figure 1.

Figure 2.

Figure 3.

IDEXX Laboratories

IDEXX is the global leader in veterinary diagnostic equipment. When a dog has a blood test, urinalysis, or cancer screen, there is a high chance that an IDEXX product is involved. IDEXX sells diagnostic instruments to vet practices, then earns a highly recurring, high-margin revenue stream from the consumables that those instruments require for years afterwards. This "razor blade" model, combined with deep integration into practice management software, makes IDEXX's revenue remarkably durable.

The company has recently launched two major product platforms: inVue Dx, a point-of-care analyser that uses AI to diagnose conditions such as ear infections and cancer from fine needle aspirates within minutes, and IDEXX Cancer Dx, a blood-based screening panel that can detect canine lymphoma and mast cell tumours up to eight months before symptoms appear. Both are scaling quickly and should support faster growth in consumables. The cytology market alone is estimated at more than 100 million procedures globally, with only a small proportion currently performed.

IDEXX started 2026 strongly reporting Q1 revenue and EPS growth of 14% and 15% respectively. Management now expect EPS growth of circa 13% in 2026, up from 11% a few months ago.

Softcat

Softcat is a leading IT value added reseller in the UK helping small and medium-sized businesses to procure the right hardware and software. Softcat operates as an extension of the sales forces of its vendor partners and an extension of the IT departments of its customers, making itself an indispensable part of the value chain.

Gross profit, the industry’s key metric for top-line growth, has been compounding at a double-digit rate for over 20 years, and we see this level of growth as sustainable as businesses prioritise technology investment to remain competitive.

Softcat announced in its most recent quarterly update that demand for its products and services remains strong as client investment in AI-related infrastructure accelerates. Importantly, Softcat has been able to meet this demand despite growing shortages of hardware components thanks to long-dated relationships with important vendors.

Management now expects mid-teens annual growth in profits, up from high single digit a couple of months ago.

Softcat’s share price has surged 35% over the past couple of weeks as the market’s “AI loser” narrative weakened.

Ferguson

From a contribution to returns perspective, Ferguson was the largest detractor in May.

Ferguson is the leading distributor of plumbing and related products in the US. The company generates 60% of its sales from maintenance and renovation projects and the remainder from new construction projects. About half of its sales are linked to the residential market and the remaining half to infrastructure.

Ferguson started 2026 well with sales and EPS in Q1 growing 4% and 9% respectively, despite weak residential demand. While the annual guidance was maintained, management is not seeing residential demand improving meaningfully, a message that was echoed by most US housing exposed companies in their outlook statements.

While Ferguson’s business is more cyclical than the average Fund holding, the company also benefits from several structural growth trends such as accelerating investment in water and energy infrastructure and construction of large capital projects such as data centres. Moderate margin expansion and ongoing share repurchases should then also help Ferguson to meet our EPS growth forecast of 8% to 12% over the coming years, without the need for a buoyant residential market.

MonotaRO

The Fund reinitiated a position in MonotaRO, a leading online distributor of MRO (Maintenance, Repair and Operating) products in Japan. The MRO category includes all those products that businesses might need to run their operations smoothly on a day-to-day basis. Examples of these products are machine spare parts, lubricants, cutting tools, safety equipment and cleaning supplies. Through its e-commerce platform and logistics infrastructure, MonotaRO offers thousands of products with fast delivery to customers, reducing the complexity and supplier sprawl that have historically made MRO procurement extremely inefficient for businesses.

MonotaRO started operations in 2000 and has been compounding EPS at an annual rate above 20% over the past decade. While the broader MRO market grows in line with the Japanese economy, the online channel, which we estimate still accounts for less than 30% of the overall market, grows faster. Within this faster-growing part of the market, MonotaRO is well placed to win share thanks to ongoing investments in its product range and distribution facilities. Growing scale and automation should also continue to support steady operating margin expansion. We view the recent share price weakness, driven by potential weakness in Japanese industrial production, as a buying opportunity.

The Fairlight View

The Fairlight investment process continues to emphasise quality and valuation-discipline above all else. The first reporting season of 2026 was a positive one for the Fairlight portfolio and reinforces our confidence in our estimates for reliable double-digit EPS growth. The Fund has only traded at approximately today’s Price to Earnings (PE) multiple twice in the past seven years - during the depths of COVID and again following the 2022 interest rate cycle. Any recovery in the PE ratios across our holdings would provide a tailwind to the returns provided by EPS growth alone. The Fairlight team is taking advantage of this possibility by increasing their personal investments in the Fund.