Menu

Close

Menu

Close

January 19, 2026

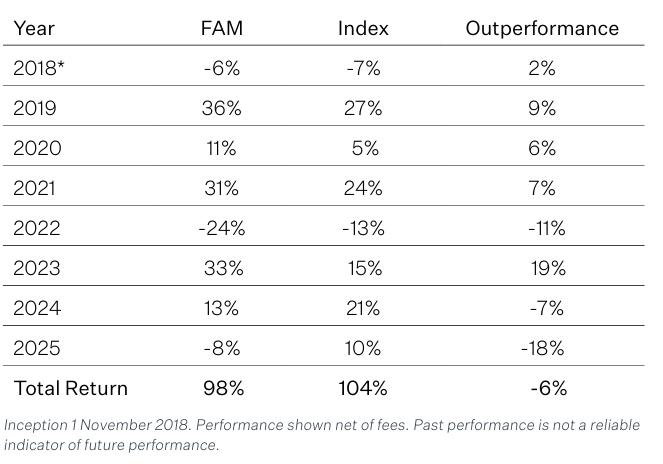

The Fund underperformed its benchmark during 2025, delivering investors a negative 8% return, compared to a positive 10% return for the MSCI World SMID Index. Since its inception in 2018, the Fund has now delivered investors 10% p.a. after all fees, in line with the benchmark. This result is disappointing, as only eight months ago, the Fund’s annualised performance since inception was 3% above that of the benchmark, in line with Fairlight’s long-term objective.

As discussed in our recent monthly reports, during the second half of 2025, two major themes have negatively impacted Fund returns. Importantly, we believe both represent temporary headwinds to performance:

1. Focusing on absolute performance, several of our portfolio companies have experienced sharp multiple contractions due to the perceived higher risk of disintermediation due to expected widespread adoption of Generative Artificial Intelligence (GenAI). We estimate that this has been an 8% hit to returns.

While we recognise that GenAI technology is potentially reducing barriers to entry to most markets, warranting a subsequent increase in valuation discount rates, we also believe that the extent of the recent ‘derating’ of these businesses is excessive given their successful track records of defending their market leaderships. We have been engaging with the management of our companies throughout the year, talking with their customers and competitors, as well as industry experts, and believe that their competitive advantages remain strong.

Most importantly, we are pleased with the operational performance of our holdings, which collectively grew revenues by 6% and EPS by 9% in 2025, a year characterised by geopolitical tensions and weak economic growth. We forecast an acceleration in these growth rates for 2026*.

2. The Fund also underperformed on a relative basis in 2025, with the benchmark returns propelled by a subset of sectors that the Fairlight strategy avoids entirely due to the lack of earnings durability. Benchmark returns were concentrated among a group of highly cyclical businesses (e.g. gold miners), interest rates-sensitive financials (e.g. banks), highly regulated companies (e.g. armaments), highly leveraged infrastructure assets (e.g. data centres) and unprofitable businesses (e.g. AI-driven nascent businesses).

While we are disappointed by the level of this year’s underperformance, we remain committed to the Fairlight investment process, believing that, longer-term, we are best served by focusing on those sectors where probabilistically we are most likely to find the high-quality operating businesses that display the earnings durability that we seek to compound wealth over time with lower levels of risk.

The Fund is now trading at a forward multiple of earnings of 19x, close to the level reached at the peak of the Covid-19 selloff. Members of the team have been adding meaningfully to their investments in the Fund and are continuing to do so.

Measuring Our Performance

The table below splits the performance of the Fund by calendar year. 2025 was the worst year of relative performance for the Fund since inception, with the Fund lagging its benchmark return by 18%.

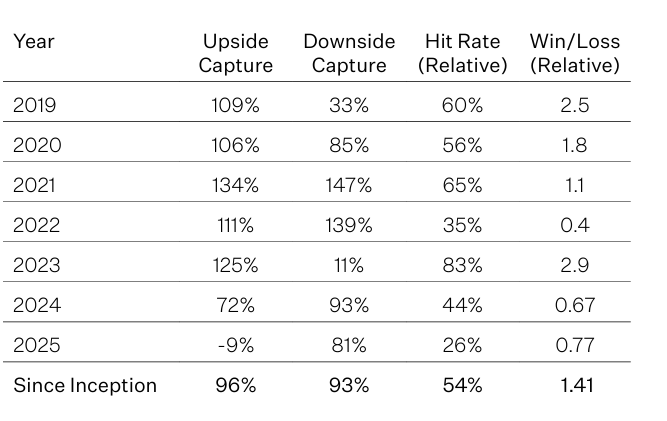

The usual additional metrics for Upside/Downside Capture, Hit Rate and the Win/Loss Ratio (for detailed discussion on these metrics, please see 2020 in Review and 2019 in Review) are provided below. Given the 18% divergence in performance compared to the benchmark these metrics are particularly poor for the year. The negative 9% Upside Capture and Hit Rate of 26% show well how the Fund has struggled over the year to keep up with the benchmark given the fundamentally different sector allocation which we discussed above.

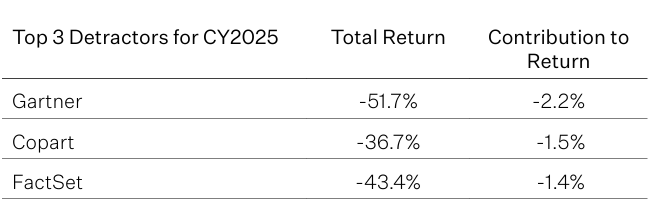

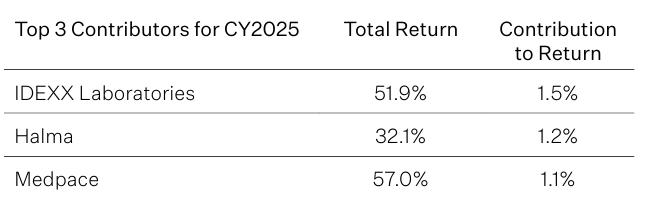

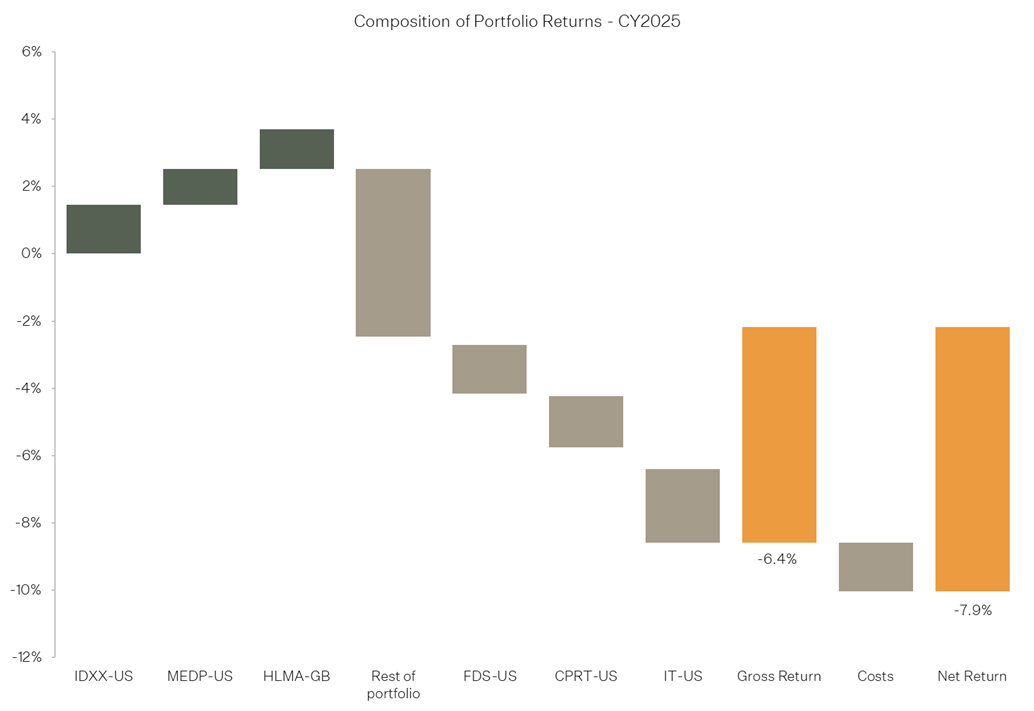

Below we provide stock-specific commentary on the top 3 detractors and contributors in 2025 (Figure 1).

Contributors and Detractors to Return

Gartner provides proprietary IT data and research to the executives of large corporations, primarily via expert conversations. For instance, Gartner is increasingly helping key decision makers to understand how AI will shape their roles and organisations. Perhaps ironically, though, many investors worry that clients will soon be less reliant on Gartner’s services as they will derive their insights mostly through Large Language Model platforms. We remain confident that Gartner will continue to be a trusted adviser in the years to come and have added to our investment in the company. Even if AI can generate good research, it is the ability to speak with a Gartner expert on-demand that is instrumental in making sense of complex topics and making expensive investment decisions. As a result, we think that the risk of Gartner being disintermediated by GenAI is low. We see management’s decision to accelerate the speed of the buyback over recent months as a positive signal (more than 5% of the company’s shares were repurchased in the second half alone). Notably, members of the management team have also been buying shares with their own money (in December, a director bought US$10m worth of shares).

Copart is a global online auctioneer of vehicles that primarily connects auto insurance companies with a fragmented base of dismantlers, used-car dealers, exporters, and individual buyers. Copart operates a two-sided marketplace where it usually sells on consignment rather than owning inventory, generating most of its revenues from service and auction fees, as well as ancillary services such as storage, transportation, title processing, and salvage value estimation. Copart’s share price has been under pressure in 2025 primarily due to two factors: 1) The cost of comprehensive insurance, which is seeing more drivers decline purchasing this insurance, and 2) Market share gains from insurance carrier Progressive, which is primarily serviced by competitor IAA. Both impacts are likely to be cyclical, with insurance premium costs moderating in 2026 and insurance companies beginning to replicate the success factors of Progressive. We have recently added to this investment.

FactSet provides financial information, data and analytics to the global investment industry through its subscription-based software. While the market is competitive, FactSet boasts over 95% recurring revenue, including deep relationships with fund managers, brokers and wealth management businesses. In 2025, FactSet posted its 45th year of consecutive revenue growth; however, its stock has sold down significantly on fears of potential AI disruption to the business model and demand from a potentially shrinking client base of investment analysts. Management has announced major investments in data and AI infrastructure in 2026, which will come at the expense of short-term margins. We believe this is the right decision. We note the business continues to grow organically, client retention exceeds 95% and senior leadership have been buying shares on-market. The Fund continues to hold shares in FactSet.

IDEXX Laboratories operates a highly attractive recurring revenue, razor‑and‑blade business model centered on companion animal diagnostics. The company places in‑clinic analysers and imaging systems with veterinary practices at relatively low upfront margins to drive long‑term, high‑margin revenue from consumables, lab tests, software, and services. Veterinarians use IDEXX’s installed base of instruments, reference labs, and cloud software as an integrated workflow, generating ongoing demand for reagents, single‑use test kits, and reference‑lab testing that represent most of the revenue and provide strong visibility and pricing power. IDEXX is benefitting from years of AI-enabled R&D spend that is resulting in an acceleration of market share and revenue growth. While the Fund continues holding IDEXX, we have recently reduced our position size based on valuation.

Halma consists of over 50 manufacturers operating in global niches within the safety, environmental and healthcare sectors. Halma’s diversification, focus on differentiated products and exposure to structurally growing markets have allowed yearly profits to compound at a 15% rate for more than four decades, with low variability. We believe Halma is exceptionally well-managed and expect this growth to continue. Despite Halma’s share price rising 32% this year, its valuation remains reasonable given the durability and quality of its growth.

Medpace is a global, clinical contract research organisation (CRO) based in the US. The company provides complex clinical development services to the biotechnology, pharmaceutical and medical device industries. The company has a differentiated operating model that is end-to-end, partnering with customers at the initiation of the clinical trial and navigating all subsequent phases, benefiting from highly experienced staff and proprietary software. Medpace has a niche focus on small to mid-sized companies and a reputation for best-in-class trial execution where successful outcomes are material to their clients who manage high cost and long duration projects. Long-tenured management have built a 30-year track record of positive organic growth and industry leading operating margins where 2025 has been no different, the business benefiting from market share gains and durable industry growth tailwinds including supporting demand for improved diagnosis and drug development. Following a strong earnings multiple re-rating, we have recently reduced our position size in Medpace.

Portfolio Changes

Portfolio turnover in 2025 was 26% and as a result, the total cost paid in brokerage equated to only 0.04% of the Fund. Portfolio changes are generally driven by two factors: 1) valuation becoming unattractive or 2) identifying mistakes or thesis drift. Fairlight is of the view that once we have found a high-quality business which is compounding earnings it is best not to interrupt this process unnecessarily with high turnover. This approach has a secondary benefit of keeping transaction costs low and deferring taxes for our investors.

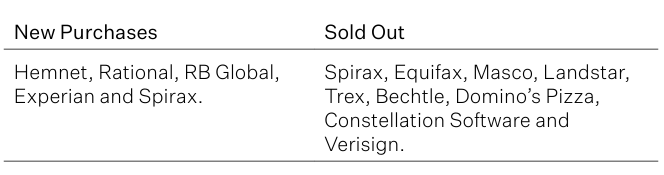

Over the year we exited 9 investments, 4 due to thesis drift (Domino’s Pizza, Landstar, Trex and Spirax) and 5 due to valuation (Verisign, Constellation Software, Equifax, Masco and Bechtle). We made 5 new purchases (Hemnet, Rational, RB Global, Experian and Spirax). Spirax was sold earlier in the year and repurchased recently after additional research was completed.

The Fairlight View

As the Fund enters 2026, it has an operating margin of 29%, cash conversion of 95%, Net Debt/EBITDA of 0.4x and is trading on a valuation of 19x forward earnings. Our estimates are for portfolio earnings growth of 12% in 2026*, which is in line with the historical growth delivered by the Fund.

Figure 1.

*The above figures are based on internal forecasts. While due care has been used in the preparation of forecast information, actual outcomes may vary in a materially positive or negative manner and should not be used as an indication of future performance.